Below is an update on how the lower middle market performed inQ3 2025.

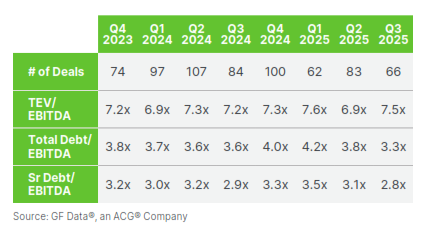

I know you two lived through many cycles. This quarter was one of those sideways moments that still carried a few surprises once you dig into the numbers. The headline is that transaction activity slowed again. 66 transactions were reported to GF Data in the quarter, down from 83 in Q2 2025. Some of this is due to the usual summer slowdown, while some of it is attributed to buyers being more cautious. They are taking their time, especially since financing is still more expensive than it was a few years ago. If you hear someone say the market is soft, this is what they mean. Fewer closed transactions, more hesitation, and a lot of standing around waiting for clarity that never seems to come when you want it.

Here is the part you probably did not expect. While the number of transactions decreased, valuation multiples increased. The average multiple was 7.5 times Adjusted EBITDA, representing a notable rebound from the 6.9 recorded in Q2 2025. This does not mean every company is suddenly worth more. What it means is that the companies that did trade were stronger, bigger, and able to support more debt. Buyers were paying up for scale and steadiness and passing on anything that felt messy or unstable.

Source: GF Data, an ACG Company

Lenders pulled back again. Total debt in transactions dropped to about 3.3 times Adjusted EBITDA. Senior debt decreased to 2.8 times Adjusted EBITDA vs 3.1 in Q2 2025. A quiet tightening that shows lenders are careful. They are choosing their spots and leaning toward larger, safer situations. Smaller transactions are still being completed, but they no longer receive the same favorable leverage terms as they did in the past.

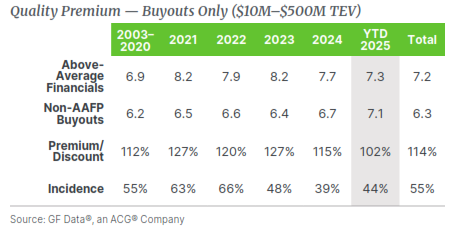

Another point you would appreciate is that the premium for better-performing companies nearly disappeared. Usually, the strongest companies get noticeably higher multiples. This time, the difference between above-average companies and everybody else was only 2%. Buyers seem to be saying that in this environment, they will pay more for size and clean financing than for perfection. That tells you a great deal about how lenders are behaving and the significant role financing plays in today’s transactions.

Source: GF Data, an ACG Company

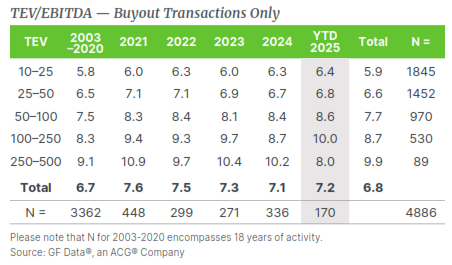

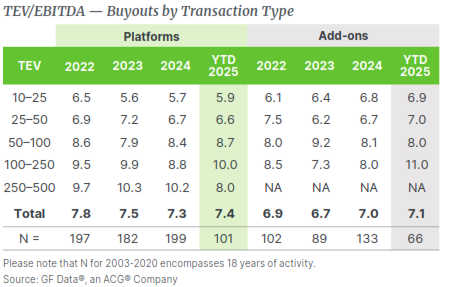

There was also a clear difference by transaction size. Companies worth $100 to $250 million saw the largest jump in valuations. They were the ones pulling the averages up. The smallest companies remained relatively unchanged. The spread between transaction sizes has widened to approximately 3.6 times Adjusted EBITDA. For example, a transaction with a total enterprise value (TEV) of $10-25 million resulted in 6.4 times Adjusted EBITDA, whereas a transaction with a total enterprise value of $100-250 million yielded 10.0 times Adjusted EBITDA. To put it in plain language, bigger businesses are more valuable because they can handle the interest burden and lenders trust them more.

Source: GF Data, an ACG Company

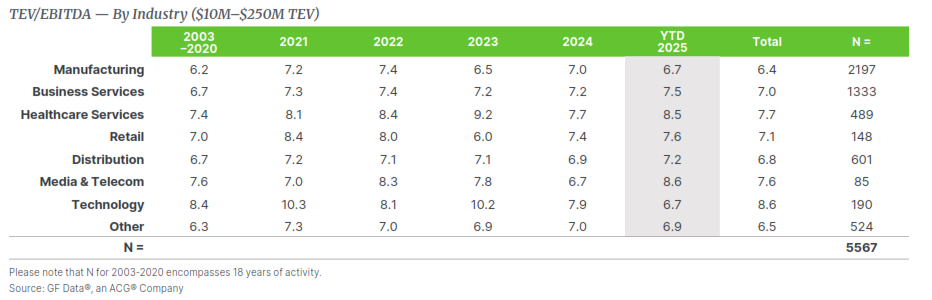

By industry, business services continued to look healthy at 7.5 times Adjusted EBITDA. Distribution and manufacturing traded at 7.2 times and 6.7 times Adjusted EBITDA, respectively. Healthcare is strong at 8.5 times Adjusted EBITDA.

Source: GF Data, an ACG Company

The quarter also showed fewer add-ons as a share of transactions, although they remain a significant part of the market. This usually means that financial sponsors (private equity, family offices, independent sponsors) are choosing to buy larger platforms when they find something strong, rather than stitching together smaller pieces. Part of this is timing, part is strategy, and part is the desire to deploy capital in one clean stroke instead of a series of smaller acquisitions.

Source: GF Data, ACG Company

If you zoom out, the story of Q3 2025 is simple. Fewer transactions, higher prices for companies that have scale, and less reward for perfection. More reward for being big enough to support the financing. Cautious lenders are still working through the reality of high borrowing costs and uneven credit conditions.

Slow quarters rarely last for an extended period of time because businesses eventually need capital, and owners eventually want liquidity. I will send you the next update when Q4 2025 comes out. Until then, I hope this helps you see the larger picture in a simple way. Even when the market feels sluggish, there is always a story in the numbers.

Subscribe to our Newsletter

Sign up for the latest industry insights from True North Mergers & Acquisitions.