GF Data recently published its Q2 2025 Private Capital Markets report. It’s one of those publications full of numbers and charts that most people would scroll past. Still, I need to take my time with it because it shows what’s actually happening in the private companies market, where family and founder-owned businesses like yours get bought and sold.

GF Data collects information directly from private equity firms that buy companies in the lower middle market. These are real, verified transactions, not surveys or opinions. Most of the businesses in the report have between $2 and $25 million in Adjusted EBITDA, which is the range where most long-standing private companies end up when they reach a certain size and stability.

There was a small rebound in transaction activity in Q2 2025 when compared to Q1 2025. 81 reported transactions in the quarter, marking an improvement over the slow start to the year. Overall, we are still about 30% below where we were last year. Buyers are being selective, moving slowly, and focusing on the cleanest, best-prepared companies.

The average multiple dropped from 7.6 times Adjusted EBITDA in the first quarter to 6.8 times in the second. That might sound like a small shift, but in this market it’s significant. It means buyers are paying less, even for quality companies. The gap between the top-performing companies and the rest has also narrowed. In the past, an exceptional company might sell for a full Adjusted EBITDA multiple higher, but right now, even the best-run businesses are closing only slightly above average. Buyers aren’t paying for potential, they are paying for certainty.

Source: GF Data, an ACG Company

Debt availability plays a big role in valuations. The average transaction carried 3.8 times Adjusted EBITDA in total debt, with senior debt at 3 times Adjusted EBITDA. That is lower than in recent years and reflects a cautious lending environment. If buyers can’t borrow as much, they can’t pay as much. It’s not a lack of interest, it’s a matter of financial reality.

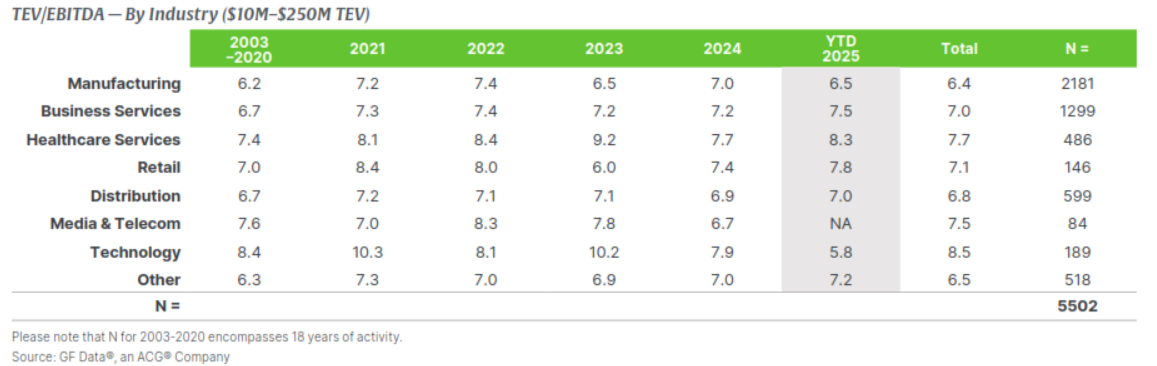

By sector, healthcare continues to lead with valuations around 8 times Adjusted EBITDA. Business services hold steady in the mid-7s, while manufacturing has softened to around 6.5 times Adjusted EBITDA. The market is rewarding predictability, recurring revenue, and low capital intensity. Buyers still prefer solid industrial companies, but they are scrutinizing every line item before they stretch on price.

Source: GF Data, an ACG Company

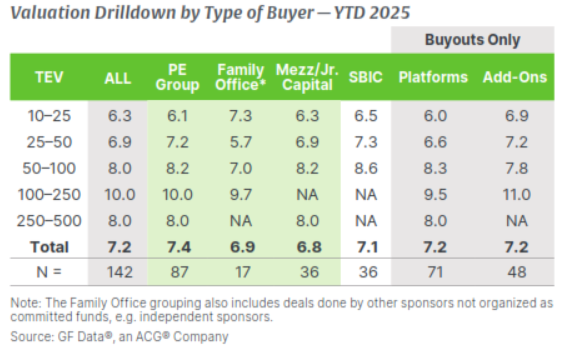

Another notable theme is that nearly 40% percent of all buyouts this year have been add-on acquisitions rather than new platform transactions. Add-ons continued to command higher valuations than platforms in the lower tiers, but the overall trend changed in Q2, with platforms and add-ons receiving equal valuations at 7.2 times Adjusted EBITDA. A platform acquisition is when a private equity firm buys a company to serve as its entry point into a new industry. It becomes the main business around which future growth is built. An add-on acquisition is when that same firm buys another, usually smaller company, to combine with one it already owns. Add-ons expand the existing business by adding customers, products, or market reach. That tells you how cautious investors are. They prefer to expand something they already know and control rather than take on the risk of a brand-new investment.

Source: GF Data. an ACG Company

Now, all of that might sound distant and abstract, but it’s not. It directly affects any owner who is quietly thinking about selling or starting to plan an exit. When the market tightens, you can’t rely on timing or hope for luck. The difference between an average outcome and a great one comes down to process. The way the story is told, the presentation of numbers, and the management of the transaction all matter.

A disciplined and confidential sell-side process exists for a reason. It is not about formality, and it's all about control. It creates competition among buyers, it keeps sensitive information secure, and it presents the company in a way that earns confidence instead of skepticism. When buyers feel certainty, they pay for it. When they sense confusion or inconsistency, they discount for it.

Even in a relatively softer market, which really depends on what you're comparing it to, there are still buyers out there paying strong multiples for well-prepared companies. The preparation is what sets them apart. A third-party quality of earnings report, accurate financials, a clear growth story, and a founder who can explain what makes their business sustainable move the needle materially.

I know you’ve seen enough cycles to understand that no one can perfectly time a market. However, personal and business readiness are things you can control. The businesses that are organized, documented, and well-presented when opportunity comes are the ones that make the most of it.

When I read through data like this, I don’t just see valuation averages or leverage ratios. I see families like ours, people who’ve built something real, and who deserve to see its value reflected fairly when the time comes to pass it on. The market rewards preparation, patience, and process.

Subscribe to our Newsletter

Sign up for the latest industry insights from True North Mergers & Acquisitions.