2025 Summary:

· Lower middle market: Cautious, volume down 23% from 2024.

· Valuations: Steady, average 7.1x Adjusted EBITDA for 2024 and 2025.

· Buyer behavior: Cautious, lower debt levels led to increased equity contributions and skeptical, longer due diligence.

· Market segments: Smaller transactions saw larger declines. Healthcare and business services had the highest Adjusted EBITDA multiples at 8.5x and 7.4x, respectively.

The GF data report for Q4 2025 confirmed what we saw in the market over the last year. Going into 2025, there was a lot of talk that this would finally be the year where M&A fully “came back.” Interest rates had stabilized, lenders were slowly loosening, and many business owners had been sitting on the sidelines for a couple of years, waiting for a better moment. The expectation was that deal volume would rebound, and buyers would start competing again, as they did in 2021. What happened was something different. The market did not fall apart, but it also did not regain the energy that marketplace participants expected. It stayed cautious, uneven, and slower than usual, with buyers taking their time and moving only when they saw something they trusted.

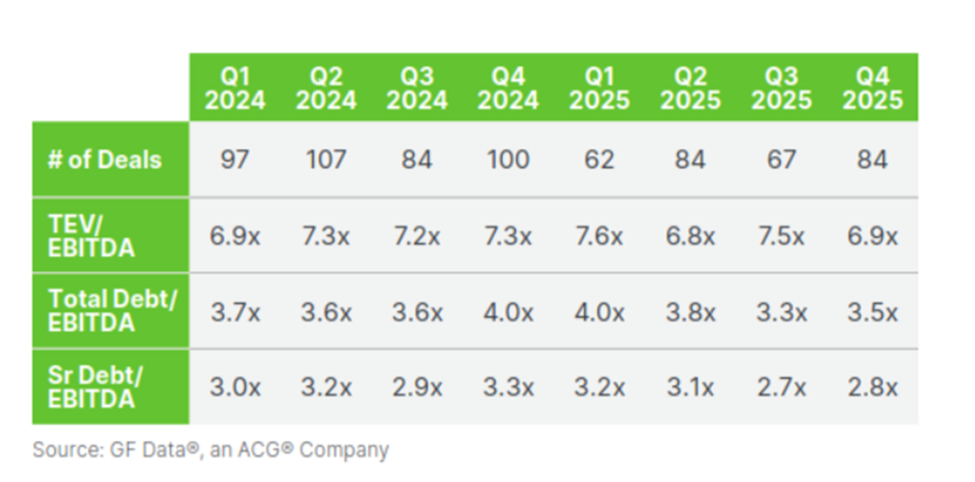

GF Data indicates that activity picked up a bit at the end of the year, with 84 transactions completed in Q4, matching Q2 2025 and improving from Q3 2025. When you zoom out and look at the full year, the bigger picture is that transaction volume in 2025 was still down meaningfully. GF Data tracked 297 completed transactions for the year, which is down 23% from 2024 and essentially flat compared to 2023. The important point is that transaction volume remains far below the post-COVID-19 peak, and GF Data notes that 2025 finished 41% below the 2021 high. That is a very clear signal that, even though buyers are active, they are not rushing or chasing volume for the sake of consummating transactions.

Valuations held up better than many marketplace participants would expect given how much transaction volume declined. In Q4 2025, the average purchase price multiple dropped to 6.9x trailing Adjusted EBITDA, down from 7.5x in Q3 2025, which is a noticeable move quarter-to-quarter. On a full-year basis, data shows average valuation multiples for 2025 held steady at 7.1x Adjusted EBITDA, basically unchanged from 2024. The market is not “cheap,” and buyers are not getting bargains across the board. Capital is still there, private equity still has money to deploy, and quality businesses are still being valued at respectable multiples. What has changed is not the price level as much as the mindset of the buyer. The market has become more selective, more risk-sensitive, and much less forgiving of anything unclear in the story.

Source: GF Data, an ACG Company

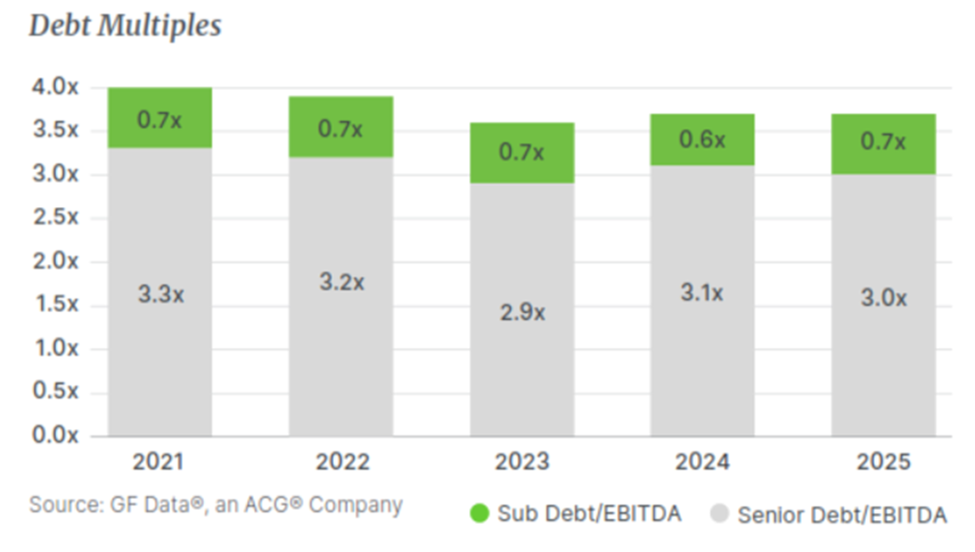

One of the main reasons the market is behaving this way is financing. Leverage data shows that debt levels remain lower than what buyers could access during the post-Covid peak years. For 2025, average total debt was 3.7x Adjusted EBITDA, slightly down from 2024, and average senior debt was 3.0x Adjusted EBITDA, down from 3.1x the prior year. That might look like a small shift, but it is enough to change transaction dynamics materially. When lenders are more conservative, buyers need to contribute more equity, and when buyers contribute more equity, they start thinking differently. They slow down, they diligence harder, and they negotiate more aggressively around working capital, customer concentration, retention risk, capex needs, and management depth.

Source: GF Data, an ACG Company

That is exactly what we have seen in real processes. We have entered two due diligence processes for our sell-side clients that generate between $10 and $20 million in Adjusted EBITDA in August 2025. After 6-8 months of in-depth due diligence and negotiations, one transaction was closed in February and the other is scheduled to close in mid-April. That’s 6-8 months of due diligence versus the typical 3-4 months of due diligence. In 2021, a buyer could justify stretching on price because cheap leverage made returns easier to achieve. In 2025, leverage is available, but it is not abundant, and lenders are still underwriting carefully. That makes the buyer’s margin for error smaller, and the seller feels that in the form of tougher diligence and tighter terms.

Another theme from the report, consistent with reality, is that the lower end of the market is under greater pressure than the upper end. Smaller transactions, particularly those in the $10 million to $25 million enterprise value range, saw valuation multiples decline more sharply late in the year. The quarterly breakdown shows this tier fell from 6.4x Adjusted EBITDA in Q3 2025 to 5.7x in Q4 2025, representing meaningful compression. Larger transactions, especially in the $100 million to $500 million range, continue to show more resilience, partly because larger companies have more financing options, deeper management teams, and generally a more institutional profile that buyers and lenders trust. In a cautious market, scale matters, and the market is still rewarding companies that seem to be easier to underwrite.

The report also reinforces something we talk about frequently, which is that sector matters more than ever. GF Data’s industry data shows healthcare services averaging 8.5x Adjusted EBITDA in 2025, business services averaging 7.4x, distribution averaging 6.9x, and manufacturing averaging 6.6x. The spread is not small and indicates that buyers are still paying premiums for asset-light businesses with predictable revenue, customer behavior, and lower capital requirements for growth. Business services continues to stand out, with the category achieving the highest valuation on record and remaining near peak deal volume compared to 2021. Even when the broader market slows, buyers still show up for the right business model. Manufacturing, on the other hand, saw both transaction volume and multiples decline, attributable in part to margin pressure and uncertainty in consumer-facing manufacturing tied to tariffs and pricing power.

One part of the report that I think business owners should pay special attention to is “quality premium.” Historically, there has always been a meaningful premium paid for the best businesses. Strong growth, strong margins, low customer concentration, clean financial reporting, and a management team that can run the business without the owner doing everything. Those companies were usually rewarded with a higher multiple, sometimes by a full turn or more in the Adjusted EBITDA multiple. In 2025, the premium has narrowed, with above-average performers trading at 7.2x Adjusted EBITDA and non-above-average performers at 7.0x. That is essentially no premium at all, and this was the lowest full-year quality premium in GF Data history. Many businesses that would have qualified as “above-average” in prior cycles fell just short due to slower revenue growth, even though margins remained strong and cash flow stayed durable. In this market, buyers are rewarding stability and durability over growth for growth’s sake, and as a result, the gap between a “great” company and a “good” company is narrowing in the data.

That does not mean quality does not matter. This means buyers are no longer paying for ambition and projections as they once did. They are paying for cash flow they can trust, revenue they can underwrite, and business models that feel predictable even if the economy stays choppy. The market is less impressed by a high-growth story if that growth appears fragile, single-customer-driven, or reliant on a single key person. In 2025, the premium is being paid for durability, not excitement, and that is a subtle but important shift.

The leveraged recapitalization is becoming a more meaningful tool for financial sponsors. Recaps represented 7% of completed transactions in 2025 and carried the highest average valuation at 7.7x Adjusted EBITDA. This is happening because many private equity firms are holding companies longer than they expected. They are not getting the clean exits they assumed they would get when they bought businesses in 2019 through 2021. So instead of selling, they recapitalize, refinance, take some money off the table, and buy more time. This matters because it shows that even sophisticated buyers are adjusting to the reality that the exit market is slower and requires patience.

The market is still open, but it has become much more selective and much more disciplined. Buyers are still willing to pay strong multiples, but they want to know exactly what they are buying, understand the risks, and feel confident that the business will perform the same way after the owner steps back. That is why you can still see 7.1x Adjusted EBITDA average multiples for the year, even while transaction volume is down sharply. The transactions that are getting done are the ones where the seller is prepared, the financial story is clean, and the business feels “safe.” The transactions that fail are not necessarily bad businesses, but they are businesses where the buyer cannot get comfortable quickly, where diligence drags, where the reporting is messy, or where too much depends on one relationship, one customer, or one person.

From a practical standpoint, this is the type of market where preparation matters more than timing. Our prospective sell-side clients frequently ask if they should wait for a better market, but the truth is that for most businesses, the best time to sell is when the company is running well, margins are stable, and the business feels organized. Buyers are still paying up for businesses that feel durable, even in a slower year, but they are not overpaying for businesses that feel uncertain. If an owner is considering a sale in the next two to three years, the smartest move is to begin preparing quietly now, even if the decision is not final. That means cleaning up financial reporting, understanding and normalizing working capital, reducing customer concentration where possible, building a management layer that can sustain the business, and being honest about which parts of the company are truly repeatable and which depend on the owner.

This is also a market where a business owner needs to be careful about assuming the multiple will take care of everything. A 7x Adjusted EBITDA multiple may seem attractive, but if the business has weak reporting, unclear EBITDA adjustments, or working capital swings, the seller could lose real value through structure, escrow, earnouts, or post-closing adjustments. The transactions that close smoothly and at strong valuations are those where the business is presented clearly and credibly from the outset, because in a cautious market, trust is one of the most valuable assets a seller can create. That trust comes from preparation, not from storytelling.

The market is stable but not particularly generous. Pricing remains steady, and buyers are exercising caution. Although transaction volume has decreased, available capital persists. While leverage is accessible, lenders are taking a conservative approach. Certain sectors, especially business services and healthcare, continue to receive positive attention, while more cyclical and margin-sensitive sectors are under greater scrutiny. Most importantly, buyers are still buying, but they are buying what they can underwrite confidently. That is what 2025 was, exactly what you would expect in a world where money is no longer “cheap”.

Subscribe to our Newsletter

Sign up for the latest industry insights from True North Mergers & Acquisitions.